Apple will report earnings after Tuesday’s close, and I expect the stock to get short-squeezed higher no matter what the news. This has already occurred in a few of the highly manipulated “lunatic stocks” held mainly by institutions, including Google, Netflix and Facebook. With regard to AAPL, my longstanding target for the stock, currently trading for around 129.25, is 144.26, but the bullish outlook comes with a warning. For further details and a precise technical look at AAPL’s vital signs ahead of the earnings announcement, check out this five-minute recording. It was prepared Friday afternoon with the stock rebounding from a weak opening that would have fooled bulls and bears.

Apple will report earnings after Tuesday’s close, and I expect the stock to get short-squeezed higher no matter what the news. This has already occurred in a few of the highly manipulated “lunatic stocks” held mainly by institutions, including Google, Netflix and Facebook. With regard to AAPL, my longstanding target for the stock, currently trading for around 129.25, is 144.26, but the bullish outlook comes with a warning. For further details and a precise technical look at AAPL’s vital signs ahead of the earnings announcement, check out this five-minute recording. It was prepared Friday afternoon with the stock rebounding from a weak opening that would have fooled bulls and bears.

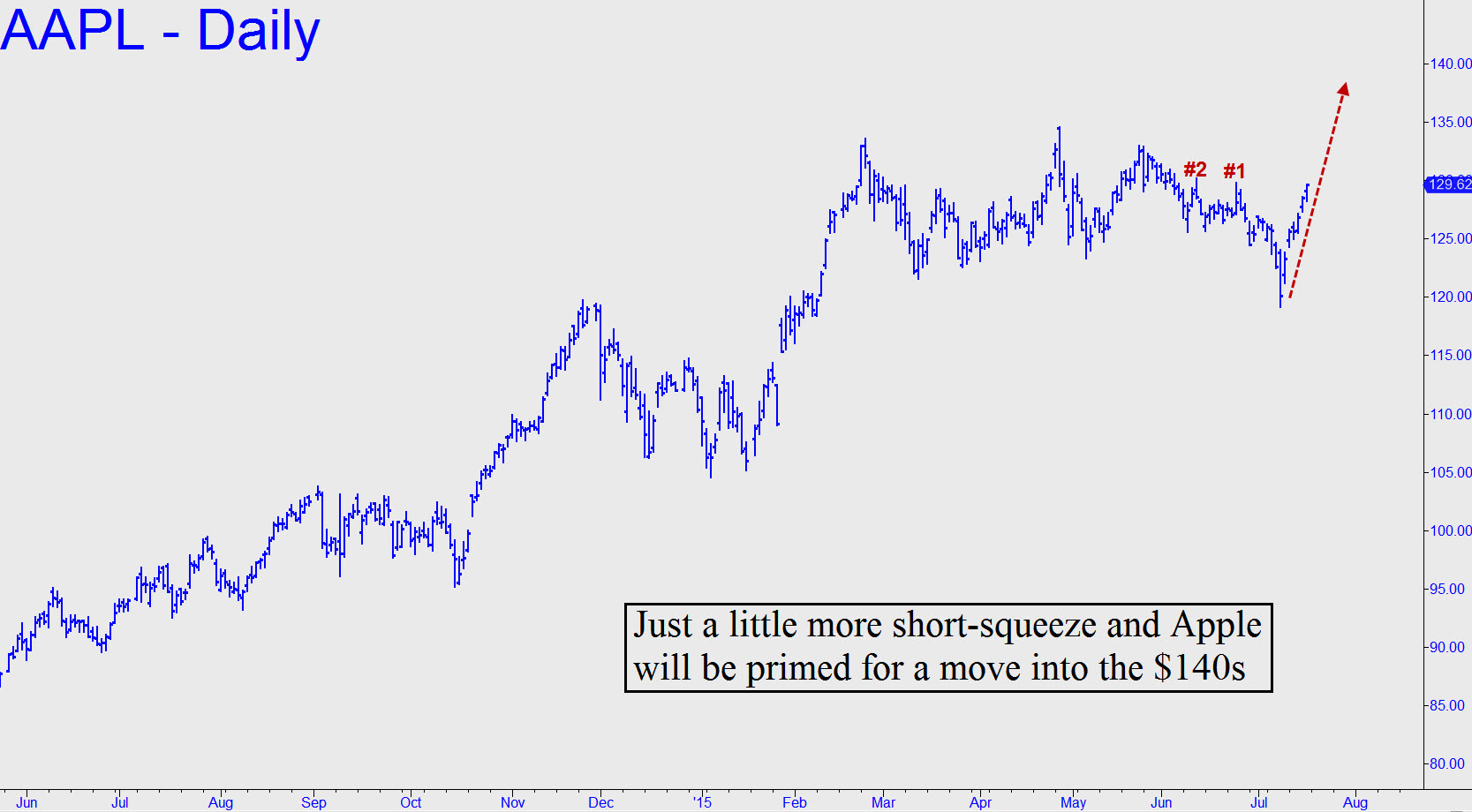

My recent commentary on Apple has emphasized the negatives, since the stock has shown no net price gain since February. Does this suggest that Apple, corporately speaking, has lost its mojo? Although it’s too early to say, AAPL’s charts suggest that a cautionary outlook is warranted. The $10 selloff that occurred between June 24 and July 9 generated the first bearish impulse leg we’ve seen on the daily chart since 2012. The earlier decline was part of a bear market that saw the stock fall by 44%. For the moment, the good news is that the technical damage done by the recent weakness would be negated by a move above May’s record high at 134.54. That is a mere $5 above Friday’s settlement price — a distance that could easily be covered by week’s end if Tuesday’s earnings announcement catalyzes even a moderate short squeeze. Were that to occur, the 144.26 target noted above would be in play, although there would be two additional impediments, both of them minor Hidden Pivots, at 134.18 and 141.56 respectively. Please note that, according to my proprietary forecasting system, when a Hidden Pivot resistance or support is easily exceeded, it is usually a reliable indicator that the next in the sequence will be achieved. Whatever happens, the 144.26 target is sufficiently compelling that it could mark a very important top.

Apple’s Successes Have Matured

If so, what fundamental factors might explain it? For one, there is the possibility that Apple’s margins for iPhone may have peaked. With the recent report that iPhone accounts for 80% of all profits globally in the smart phone category, profits don’t have much room to improve. The company has benefited from a consumer cult that doesn’t seem to mind paying up for Apple hardware, regardless of price. As a result, unit sales for iPhone have grown even as prices have risen. This is a singular anomaly in the retail word, but whether it can last is arguable. My hunch is that it’s only a matter of time before competition from Xiaomi in particular begins to eat away at AAPL’s astounding profit margin. The company already produces a cell phone that does everything an iPhone can do for half the price. It is only a matter of time before the Chinese manufacturer offers a phone for under $100 that can equal or top the $600 iPhone feature-for-feature. iPhone users will already know that battery life in particular is one performance category in which Apple phones are particularly vulnerable. One other factor is bound to hurt Apple more than any of its competitors: global recession. Bull markets do end, and when this one, which has been chugging along since March 2009 sputters out, the economic fallout will be particularly hard on sales of Apple’s pricey hardware.

Streaming music is another area where AAPL will be challenged by competitors who have been in the game for years. One of the most formidable of them, Spotify, has put the Sunnyvale company in the unfamiliar position of having to play catch-up. Spotify correctly saw the market shifting from “owned” music to streamed music; Apple sat by for 12 years and stuck with the old model. Now, it will require a very deft blending of content from a variety of sources and media for Apple to recoup the segment of the market it effectively ceded to Spotify. Will Apple be able to dominate with content that is neither hardware- nor software-specific? The jury is still out, but they will not have the iTunes advantage of being the first to exploit a particular way of delivering content.

Some have even argued that Apple should get out of the computer business entirely, the better to focus on the Next Big Thing — whether it be energy storage, or driverless cars, or…? In this view, Apple would be relinquishing its hold on a 20th Century technology and products in order to achieve world-beating success in new ones. Are they up to the challenge with Steve Jobs gone? Perhaps that question has been weighing on the minds of investors who have stalled the steep rise in AAPL shares in recent months.