(Following is the fourth in a series of articles on gold by Chuck Cohen, a financial consultant and lifelong resident of New York City.)

Recently I discussed some of the reasons investors often fall short. Today I want to help bring clarity to your investment goals and also explain why gold should hold a central place in your portfolio. If you succeed in these two areas, you’ll not only prosper, you will also be prepared for the incredible changes and shocks that I believe are coming.

As Richard Russell always stresses, succeeding in the stock market is a lifetime learning process. At age 84 or so, he is still working diligently at it. As we have all learned, making money in the stock market is not as easy as the hucksters would have us believe. Success comes not just from market knowledge but from learning from our mistakes. And it is critical to acknowledge that we all make mistakes. To succeed also includes knowing ourselves, especially the emotions which often rule our decisions. It can be just as important to avoid a disaster or to get out of a potential one than to have a successful trade. Just as in baseball, we aim to have a high batting average and to avoid deep slumps. And as an aside, (speaking from experience), this invariably means making sure your spouse is comfortable with your finances.

Because of these issues, we need to lay a foundation from which we can look at the markets, especially gold, intelligently and dispassionately. Once we have done so, we will get into more detail. Please excuse any overlaps or repeats as we go along. Some might be intentional, some not.

Gold as a Core Investment

When I began contributing essays to Rick’s Picks recently, I didn’t know how familiar readers were with gold, particularly the idiosyncrasies of various mining companies. Judging from the e-mails and comments I received, however, I have inferred that many of you are fairly knowledgeable and active in bullion. Even so, let’s review some fundamentals.

As I mentioned earlier, gold does not require an all-or-nothing commitment, and it needn’t be a stand-alone investment. However, it should hold an essential position in these uneasy and uncertain times. It must be considered within the overall economic landscape that also includes your personal situation plus your other investments.

Last week we looked at gold as we would a house or an insurance policy. Now I want to present it as a core investment relative to your overall strategy. We’ll also consider gold as a speculative vehicle. In future articles I will continue to underscore that we now live in a period vastly different from all others before us. The financial and geopolitical ground around us is shifting, and before long, great, irrevocable changes will arrive. Therefore, our approach to our lives, and especially to our finances, must stress preparedness so that we can adapt to these changes. What has been successful in the past is not likely to work in the future. Having witnessed the decimation of such hallowed financial institutions as Bear Stearns, Lehman Brothers and AIG, can we logically assume the worst is behind us? Surely not. Let’s look at four factors that should deepen our commitment to gold.

I. The World Landscape Is Shifting

Despite the spin from Washington and the financial media that things will somehow work out, this requires the kind of faith that I – and probably many of you — just don’t have. Given the tumultuousness of the last decade, only an ostrich would buy into this sunny assumption.

A quick list of our problems is not meant to be depress you so that you can’t sleep. But it reflects the hard reality of our nation’s condition, to wit: 1) unlike China, we have no savings set aside, either by households or by government at all levels. Meanwhile, we are trying to induce a debt strapped-consumer to spend even more by going deeper into hock; 2) revenues and tax collections at all levels of governments are collapsing; 3) infrastructure is deteriorating and in dire need of rebuilding; 4) Social Security and Medicare are drastically underfunded even as Baby Boomers approach retirement; 5) corporations face vast unfunded pension liabilities; 6) all of these problems will contribute to a bleak employment outlook; and, 7) our only solution at this point has been to stimulate through the injection of trillions of paper dollars. This cannot hide the fact that America is technically bankrupt.

The dollar, once the world’s great currency, is under close scrutiny by overseas creditors. They are considering a shift away from dollars, which would result in either a profound dollar weakness, dramatically higher interest rates, or both. It is almost unimaginable that the once great creditor nation of the United States is now at the mercy of, what were until recently considered, underdeveloped countries. Please read Julian Phillips’ latest article on China, the yuan and the dollar. He is a very perceptive observer.

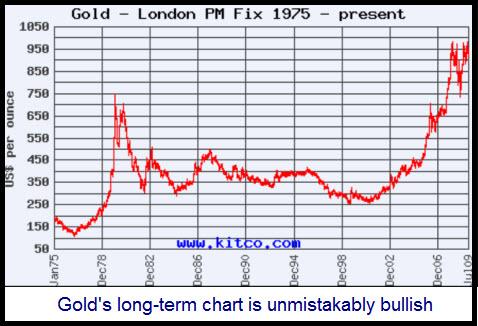

My point is this: Is it logical that we will somehow muddle through our mess, and by faith believe that these problems can, through the issuance of money out of thin air, be solved or just disappear? I don’t think so. A more reasonable conclusion is that America is on a elongated down slope. As a consequence, the price of gold will continue to increase, and most likely accelerate.

II. Personal Financial Risk Is Increasing

What is your personal financial situation, and what are your expectations? How might these things be affected by your age, health and family considerations?

* Is your trading or investment money in an IRA or in a taxable trading account? That’s a very important point to consider.

* Do you wish to take risk because you are young, or do you wish to play it safe? Perhaps you are retired and are on a limited budget?

* Is your employment secure?

* Do you have debts that you must pay off?

* Are you putting children through school?

These issues affect how you can approach gold. We’ll get into many of these at a later date.

III. Gold Alternatives Have Soured

I assume that you have some savings invested in different vehicles. Let’s look very briefly at some of them.

Most investors still believe that stocks, bonds and even real estate are the safest and best places to be for the long-term. Because this reflects the popular wisdom and is reinforced constantly by the financial media, we tend to continue to stay where we feel most comfortable.

But in retrospect, the past ten years have been unkind to stocks and real estate. The terrific returns that were quoted back in 2000 have collapsed and we sense that things will get worse before they get better. Indeed, just because stocks and real estate have been severely hit, can we assume, as most analysts do, that the worst must be over? Or are we in a period like 1930-31, when it appeared that the stock market was righting itself, only to fall to a full decline of 90%?

And bonds? They have fared much better in this decade, but given the very extraordinary infusion of monetary easing and the immense financing that will be required in Bailout Nation, isn’t it likely that rates are about to rise? In the 1970s, in a similar monetary environment, the bond market was a disaster, with short term rates soaring to over 20%. To reiterate: The key to success is to understand the big picture, to position oneself accordingly and to try to be prepared for the unexpected. The recent historic monetary events show that sudden shocks strike without any warning.

IV. Brace for the Worst

Finally, I must include a huge “What if?” By this I mean the financial equivalent of 9/11. This is hardly a stretch when we consider how quickly Bear Stearns vanished in the mire of financial derivatives. Recall that the firm was alive and kicking at $62 on March 10, 2008; four days later it was gone. I believe that the next shock may come with even less warning, and this time with no safety net. This is where the insurance and potential upward explosion of gold really is critical.

Conclusion

The more we delve into the world economic and political landscape, the more attractive gold becomes and the more we might wish to expand and deepen our involvement. A corollary is that you may wish to reapportion some of the alternatives. I believe in spite of sharp stock rallies and declines, bouts of market optimism and pessimism, one thing is certain: We are in uncharted water. Fiscal problems that used to be reckoned in billions now tally into the trillions. As a result, no one can predict what the outcome will be.

NEXT WEEK: Some investment possibilities, including coins, ETFs, precious-metal funds and mining shares (senior, junior and exploration).

If you’d like to have Rick’s Picks commentary delivered free each day to your e-mail box, click here.

Please comment on having gold and silver stocks in an IRA.

&&&&&

My wife and I do and I think it is the best way to go. Thanks. Chuck